The economic expenditure that must be made to buy or maintain a service or product is called cost . Marginal , for its part, is that which is on the margins, is scarce or is secondary.

The economic expenditure that must be made to buy or maintain a service or product is called cost . Marginal , for its part, is that which is on the margins, is scarce or is secondary.

In the economic sphere, the increase in the cost of production that is generated when the quantity produced increases by a unit is called marginal cost . It should be remembered that the cost of production refers to the money that must be spent to produce a service or good.

The aforementioned definition, in short, indicates that marginal cost is the increase in cost recorded when an additional unit of a certain good is produced. Put another way, marginal cost reflects the rate of change in cost divided by the change in the level of production .

Suppose a sports apparel company produces 100 pants at a cost of $500 . If, by producing 120 pants , the production cost rises to $510 , the marginal cost will be $0.5 :

Marginal cost = Cost variance / Production variance

Marginal cost = $10 / 20 pants

Marginal cost = $0.5 per pair of pants

This means that, to produce an additional pair of pants , the company in question must increase its production cost by $0.5 . If the marginal cost is $0.5 per pair of pants , and the company produces 20 more pants , its production cost will increase by $10 . On the other hand, if you start producing 50 extra pants , the production cost will increase by $25 .

This concept belongs to the fields of economics and finance , and is also known as marginal cost . From a strictly mathematical point of view, it can be said that the marginal cost must be expressed as the derivative of the total cost function, taking as reference the amount by which production has been modified, which in the previous example is represented with two dozen extra pants.

A derivative , in the field of mathematics, is understood as the function that is used to measure the speed with which its own value changes, depending on the change that its independent variable undergoes. Two more concepts are added here:

* we say that one magnitude is a function of another when its value depends on that of the other (for example, the area of a square is a function of the extension of its sides, since they must be multiplied together to give this result);

* The independent variable of a function is one to which we can assign various values within a predefined set so that it modifies the value of the dependent one. In the previous case, we could say that the area is the dependent variable, and the sides are the independent ones.

* The independent variable of a function is one to which we can assign various values within a predefined set so that it modifies the value of the dependent one. In the previous case, we could say that the area is the dependent variable, and the sides are the independent ones.

The total cost , mentioned above, is the result of adding the fixed and variable costs. Fixed ones are those that in the short term have no relationship with the production level of a company, but are stipulated in advance and are carried out regardless of performance. The variables, for their part, do depend on the amount of any variable factor used, that is, resources and production capacity.

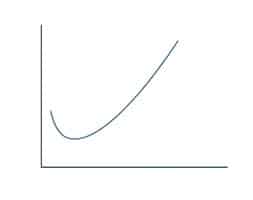

Returning to the marginal cost, it is said that its evolution should be represented with a curve shaped like a concave parabola , that is, it begins decreasing and then increases (like a letter U ), something that is justified by the law of diminishing returns , the which points out that: if a productive factor is added and the others remain constant, then the marginal increase decreases.

When observing the marginal cost curve, we notice that at its minimum point is the amount of goods that the company must produce so that the profit is minimum.